Underwriting plays a central role in how financial and insurance institutions manage risk, protect capital, and remain sustainable. Every insurance policy issued, loan approved, or security offered to the market involves an underwriting decision that balances potential returns against possible losses. As economies become more complex and data-driven, the role of the underwriter has shifted from rule-based approval to informed risk judgment supported by analytics and regulation.

In 2026, underwriting is emerging as a strong career option due to the expansion of insurance coverage, growth in digital lending, stricter regulatory oversight, and increasing use of data and technology in risk assessment. Organisations are actively seeking professionals who can combine financial analysis, risk evaluation, and compliance awareness to make sound decisions in uncertain environments.

For individuals interested in finance, economics, insurance, or risk management, underwriting offers a stable and intellectually demanding career path with clear progression opportunities. This guide explains what underwriters do, the skills and qualifications required, career pathways, and the job opportunities available in 2026.

Role and Requirements of an Underwriter

An underwriter is a professional responsible for evaluating risk and deciding whether a financial institution should accept that risk, and on what terms.

- Underwriters assess applications for insurance policies, loans, credit facilities, or securities by analysing financial information, risk indicators, historical data, and regulatory requirements.

- The core responsibility of an underwriter is to protect the organisation from excessive loss while enabling business growth. This involves determining eligibility, setting pricing or interest rates, defining coverage limits, and recommending approvals or rejections. Every underwriting decision directly affects profitability, solvency, and compliance.

- In modern financial systems, underwriters do not rely only on fixed rules. They use data analytics, risk models, industry benchmarks, and professional judgement to assess uncertainty. Whether working in insurance, banking, or capital markets, underwriters act as a critical control point between risk-taking and financial stability. Let’s look at the types and skills to become an underwriter now.

Types of Underwriters

Underwriting is a broad profession with multiple specialisations, each focused on a different type of risk and financial product. Understanding these categories helps candidates choose a career path aligned with their interests and skills.

Insurance Underwriters

Insurance underwriters assess the risk of insuring individuals, businesses, or assets. They evaluate factors such as health history, property value, industry exposure, and past claims to decide coverage terms and premiums. They commonly work in life, health, motor, property, and liability insurance.

Loan and Credit Underwriters

These underwriters evaluate the creditworthiness of individuals or businesses applying for loans. They analyse income, cash flows, credit history, and repayment capacity to decide loan approval, limits, and interest rates. They are widely employed in banks, NBFCs, and fintech lending platforms.

Investment and Securities Underwriters

Investment underwriters work with capital markets transactions such as IPOs, bond issues, and private placements. They assess the financial strength of issuing firms, market conditions, and investor demand to price and structure securities. These roles are common in investment banks and merchant banking firms.

Reinsurance Underwriters

Reinsurance underwriters assess risk transferred by insurance companies to reinsurers. Their work involves large and complex risks, catastrophe modelling, and international exposure. These roles require strong technical expertise and are typically mid to senior level positions.

Corporate and Commercial Risk Underwriters

These underwriters focus on large corporate accounts and commercial risks. They evaluate operational, financial, and industry-specific risks for large businesses and design customised risk coverage or financing solutions.

Skills Required to Become an Underwriter in 2026

Underwriting is a decision-intensive role where accuracy is crucial. In 2026, employers seek professionals who can combine financial reasoning with risk judgment, while working comfortably with data, documentation, and compliance standards.

- Risk assessment and analytical thinking: You must be able to identify what can go wrong, estimate likelihood and impact, and judge whether the risk is acceptable. This includes understanding risk drivers, red flags, and patterns across similar cases.

- Financial and quantitative skills: For credit and corporate underwriting, financial statement reading, ratio analysis, cash-flow evaluation, and basic forecasting are important. For insurance underwriting, comfort with probabilities, pricing logic, and claims trends is valuable.

- Attention to detail and documentation discipline: Underwriting decisions require strong justification. Employers value underwriters who can review forms, contracts, reports, and supporting documents carefully, without missing critical disclosures or inconsistencies.

- Regulatory and compliance awareness: Underwriters work under strict internal policies and external regulations. You must understand why compliance matters, how to follow underwriting guidelines, and how to document decisions to withstand audits.

- Communication and stakeholder management: Underwriters coordinate with sales teams, operations, actuaries, risk teams, and sometimes customers. You must communicate decisions clearly, explain requirements, and handle back-and-forth efficiently without creating confusion.

- Technology and data comfort: Underwriting increasingly uses automation, risk engines, dashboards, and workflow tools. You do not need to be a programmer, but you should be comfortable interpreting outputs from models, using underwriting platforms, and working with structured data.

- Decision-making under uncertainty: Many cases are not perfect. A strong underwriter can make balanced decisions with incomplete information, escalate when needed, and avoid both reckless approvals and unnecessary rejections.

Educational Qualifications Needed

There is no single mandatory degree to become an underwriter, but employers typically look for a strong academic foundation in finance, risk, and quantitative reasoning. The choice of education often influences the type of underwriting role you enter.

- Most underwriters begin with a bachelor’s degree in fields such as Commerce, Economics, Finance, Business Administration, Statistics, Mathematics, or Actuarial Science. These disciplines help build comfort with numbers, financial logic, probability, and structured analysis, all of which are central to underwriting work.

- For insurance underwriting, degrees in insurance, actuarial science, or risk management provide a direct advantage, especially for technical product lines. For credit and loan underwriting, finance, accounting, and economics backgrounds are more common. Investment underwriting roles often prefer candidates with strong corporate finance and capital markets exposure.

- Postgraduate degrees are not mandatory, but a master’s degree in finance, economics, risk management, or an MBA can accelerate career progression and open access to more complex underwriting roles. Advanced education becomes more valuable when moving into senior, portfolio-level, or leadership positions.

Practical exposure through internships, trainee programs, or entry-level analyst roles is often as important as formal education, as underwriting judgement develops through real-case experience rather than theory alone.

Certifications that Improve Employability

Certifications are not compulsory, but they help you stand out in 2026 because they show two things clearly: domain knowledge and decision readiness. They are especially useful if you are switching careers, applying for structured underwriting teams, or targeting higher-paying specialisations.

1) Insurance underwriting certifications

- Best for: Life, health, motor, property, liability, and commercial insurance roles

- What they help with: Policy structure, risk classification, premium logic, underwriting guidelines, claims trends, regulatory basics

- Why employers value them: You can understand products and make consistent decisions with fewer errors

2) CPCU (Chartered Property Casualty Underwriter)

- Best for: Property and casualty underwriting, especially commercial lines

- What it signals: Strong technical grounding in underwriting, coverage, and risk management

- Why it matters: CPCU is a globally recognised designation and is often valued for technical insurance roles

3) Credit risk and banking certifications

- Best for: Loan underwriting in banks, NBFCs, and fintech lending

- What they help with: Credit appraisal, financial statement analysis, cash-flow assessment, covenant understanding, documentation, compliance

- Why employers value them: You can evaluate repayment capacity and structure credit safely

4) CFA (Chartered Financial Analyst)

- Best for: Investment and securities underwriting (capital markets, merchant banking, investment banking)

- What it helps with: Valuation, financial markets, portfolio risk, ethics, corporate finance

- Why it matters: It strengthens your profile for underwriting roles linked to IPOs, bonds, and fundraising

5) Risk management and compliance certifications

- Best for: Senior underwriting, portfolio roles, and regulated environments

- What they help with: Risk frameworks, regulatory requirements, audit readiness, policy governance

- Why employers value them: Underwriting decisions must survive regulatory scrutiny and internal audits

How to choose the right certification

- If you want insurance underwriting, start with insurance institute certifications, then consider CPCU for technical tracks

- If you want credit underwriting, choose credit risk and banking-focused certifications

- If you want investment underwriting, CFA is the most relevant long-term credential

- If you want faster growth: add a risk or compliance certification after you get 1–2 years of experience

How to Become an Underwriter in 2026: Step-by-Step Career Path

Underwriting is not an overnight career. It is built through structured learning, exposure to real risk cases, and gradual development of judgement. In 2026, employers value underwriters who follow a clear progression from foundational roles to specialised decision-making positions.

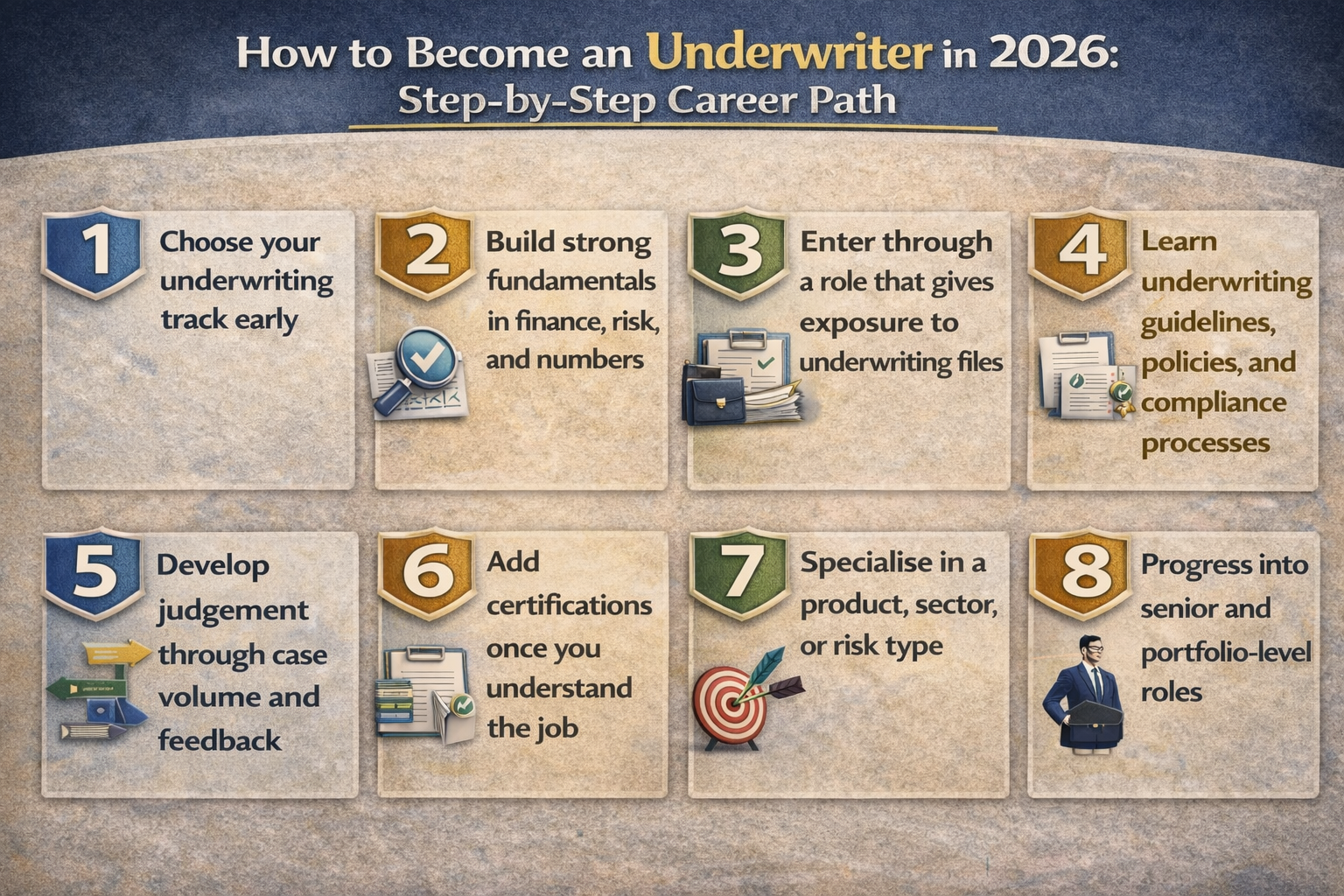

Step 1: Choose your underwriting track early

Underwriting exists across insurance, credit, and capital markets, and each track requires a different skill mix. Insurance underwriting focuses on policy coverage, exclusions, and pricing logic. Credit underwriting concentrates on repayment capacity, cash flows, and borrower behaviour. Investment underwriting deals with valuation, market risk, and deal structuring. Choosing a track early helps you focus your education and certifications.

Step 2: Build strong fundamentals in finance, risk, and numbers

Underwriting decisions rely heavily on structured thinking. You should be comfortable reading financial statements, understanding ratios, interpreting trends, and applying basic probability and risk concepts. Even in insurance roles, numerical reasoning and analytical clarity are essential.

Step 3: Enter through a role that gives exposure to underwriting files

Most professionals do not start directly as underwriters. Entry points include underwriting assistant, credit analyst, risk analyst, insurance operations executive, or policy administration roles. These positions expose you to real applications, documentation, and decision workflows, which is where underwriting learning truly begins.

Step 4: Learn underwriting guidelines, policies, and compliance processes

Underwriting operates within strict internal rules and external regulations. You must understand approval thresholds, deviation processes, documentation standards, and audit requirements. Consistency and compliance are as important as judgement in this role.

Step 5: Develop judgment through case volume and feedback

Strong underwriting judgment comes from handling a large number of cases and learning from outcomes. Reviewing rejected cases, defaults, claims, and exceptions helps you recognise patterns and improve decision quality over time.

Step 6: Add certifications once you understand the job

Certifications are most effective when combined with practical experience. At this stage, certifications help deepen technical understanding, strengthen credibility, and support movement into more complex or higher-value underwriting roles.

Step 7: Specialise in a product, sector, or risk type

Career growth accelerates when you specialise. Examples include SME or corporate lending, mortgages, health insurance, liability lines, marine insurance, or reinsurance. Specialisation leads to higher responsibility, sharper judgement, and better compensation.

Step 8: Progress into senior and portfolio-level roles

With experience, underwriters move into senior underwriter, lead underwriter, underwriting manager, or portfolio risk roles. These positions involve supervising decisions, setting risk appetite, mentoring junior underwriters, and managing overall risk exposure rather than individual cases.

Tools and Technologies Used by Underwriters in 2026

Underwriting in 2026 is increasingly technology-driven. While professional judgement remains central, tools now support faster analysis, consistency, and better risk detection. Employers expect underwriters to be comfortable working with these systems, even if they are not technical specialists.

- Automated underwriting platforms: These systems apply predefined rules, scorecards, and policy guidelines to applications. They help filter standard cases, flag exceptions, and reduce turnaround time, allowing underwriters to focus on complex decisions.

- Risk scoring and credit assessment tools: Commonly used in banking and fintech, these tools evaluate applicants using credit bureau data, transaction history, and behavioural indicators. Underwriters interpret these scores and decide when overrides or additional checks are required.

- Data analytics dashboards: Dashboards track approval rates, loss ratios, defaults, claims trends, and portfolio risk. Underwriters use these insights to improve decision quality and align approvals with risk appetite.

- AI-assisted fraud detection systems: These tools identify unusual patterns, inconsistencies, or suspicious behaviour in applications and documents. They support underwriters by highlighting cases that require deeper scrutiny.

- Document management and workflow systems: Underwriting involves extensive documentation. Workflow tools help manage case files, approvals, escalations, and audit trails while ensuring compliance with internal and regulatory requirements.

- Regulatory and compliance reporting tools: These systems help track adherence to underwriting policies, exposure limits, and regulatory norms. Senior underwriters rely on them to ensure decisions withstand internal audits and external inspections.

- Spreadsheet and financial modelling tools: Despite automation, tools like spreadsheets remain widely used for scenario analysis, cash-flow evaluation, and stress testing, especially in credit and corporate underwriting roles.

Entry-Level Jobs That Lead to Underwriting Roles

Most people do not start directly as an underwriter. In most companies, underwriting is a responsibility you earn after you understand files, documentation, risk signals, and internal policies. These entry-level roles help you get that exposure and build the foundation for moving into underwriting.

- Underwriting Assistant / Underwriting Coordinator

You support underwriters by preparing case files, checking document completeness, coordinating additional information, and updating systems. This is one of the most direct pathways because you learn underwriting workflows and decision criteria closely. - Credit Analyst / Credit Associate

Common in banks, NBFCs, and fintech lenders. You analyse borrower profiles, income, cash flows, repayment capacity, and credit reports. Over time, you start recommending approvals, limits, and conditions, which naturally leads to credit underwriting. - Risk Analyst / Risk Operations Associate

These roles expose you to risk policies, monitoring, and exception handling. You learn how risk teams evaluate quality, track portfolio performance, and identify early warning signals, which builds strong underwriting judgement. - Insurance Operations Executive / Policy Administration Associate

This role is strong for insurance underwriting. You handle policy issuance processes, endorsements, renewals, and documentation checks. You learn how products are structured and why underwriting rules exist. - Claims Associate (Insurance)

Claims work teaches you how losses actually happen and what patterns lead to payouts. This experience is valuable for underwriting because it improves your ability to identify hidden risks and price coverage appropriately. - KYC / Compliance Analyst (Banking and Insurance)

Underwriting decisions must meet regulatory and internal compliance standards. KYC and compliance roles build strong discipline around verification, documentation, and audit readiness, which employers value in underwriting teams. - Relationship Manager Support / Sales Support (Banking or Insurance)

While this is not a risk role, it builds strong product understanding and customer context. If you move from sales support into underwriting, you bring practical knowledge of customer profiles and market realities, which can be useful when combined with analytical skills.

Salary and Career Growth Prospects

Underwriting offers strong long-term stability because it sits at the core of how financial and insurance firms control risk and protect profitability. Salaries rise meaningfully as you move from supporting roles to decision-making roles, and then to portfolio and leadership positions. Growth is usually faster when you specialise in complex products, commercial accounts, or high-value segments.

- Entry-level (0–2 years): learning the workflow and building fundamentals

Typical roles include underwriting assistant, credit analyst, risk associate, or insurance operations. At this stage, compensation is driven by the company, location, and sector, but the key focus is gaining exposure to real files, documentation, and policy rules. Career progression depends heavily on accuracy, speed, and your ability to interpret risk signals. - Mid-level (2–6 years): handling cases independently and owning decisions

You start managing underwriting files end-to-end, making recommendations, and approving standard cases within defined limits. Many professionals shift into specialised product lines here (for example, mortgages, SME credit, health insurance, commercial lines). Salaries increase because your judgement directly affects portfolio quality and loss outcomes. - Senior level (6–12 years): complex risks, larger ticket sizes, and specialisation

Senior underwriters handle high-value cases, exceptions, and customised underwriting. In insurance, this could involve commercial liability, marine, or reinsurance-linked work. In credit, this often includes corporate or structured lending. Compensation improves significantly because the cost of errors is higher and the decisions require stronger expertise. - Leadership and portfolio roles (10+ years): managing risk appetite and teams

Roles include lead underwriter, underwriting manager, portfolio risk manager, or head of underwriting. Your work expands from individual cases to managing overall exposure, setting decision frameworks, guiding teams, coordinating with compliance, and improving underwriting performance through policy and analytics.

What improves salary growth the fastest?

- Specialising in commercial, corporate, or high-ticket underwriting segments

- Strong financial analysis and risk judgement track record

- Certifications aligned with your underwriting track

- Comfort with analytics tools and portfolio dashboards

- Moving into roles that combine underwriting with portfolio or risk governance responsibilities

Industries Hiring Underwriters in 2026

Demand for underwriters continues to rise as organisations place greater emphasis on structured risk management and compliance. In 2026, underwriting roles span traditional financial institutions as well as technology-driven and specialised risk firms.

Insurance companies

- Life, health, motor, property, and liability insurers are the largest employers of underwriters.

- Examples: LIC, HDFC Life, ICICI Prudential, SBI Life, Bajaj Allianz, Tata AIG, New India Assurance, United India Insurance, Star Health, Care Health Insurance.

Reinsurance firms

- Reinsurers hire experienced underwriters to assess large, complex, and catastrophe-linked risks, often with global exposure.

- Examples: Swiss Re, Munich Re, Hannover Re, SCOR, General Insurance Corporation of India (GIC Re).

Banks and NBFCs

- These institutions employ underwriters for retail, SME, and corporate credit assessment to manage default risk and portfolio quality.

- Examples: State Bank of India, HDFC Bank, ICICI Bank, Axis Bank, Kotak Mahindra Bank, Bank of Baroda, Bajaj Finserv, Tata Capital, L&T Finance.

Fintech and digital lending platforms

- Fintech firms hire underwriters to oversee risk models, handle exceptions, and manage fraud and compliance.

- Examples: Paytm Lending, Lendingkart, KreditBee, EarlySalary, Razorpay Capital, Navi, Paisabazaar.

Investment banks and merchant banking firms

- Underwriters support IPOs, bond issuances, and fundraising transactions in capital markets.

- Examples: Goldman Sachs, JPMorgan Chase, Morgan Stanley, Citi, Axis Capital, ICICI Securities, Kotak Investment Banking.

Corporate risk and treasury teams

- Large corporations employ underwriting-style risk professionals to manage insurance coverage, counterparty risk, and financial guarantees.

- Examples: Reliance Industries, Tata Group companies, Aditya Birla Group, Larsen & Toubro, Mahindra Group.

Third-party underwriting and risk service providers

- These firms provide outsourced underwriting, credit assessment, and risk analytics services to insurers and lenders.

- Examples: EXL, Genpact, WNS, TCS, Accenture, Capgemini.

Challenges and Responsibilities of the Role

Underwriting is a high-responsibility function where decisions have long-term financial and regulatory consequences. While the career offers stability and growth, it also demands discipline, accountability, and strong judgment.

- High accountability for decisions

Every approval, rejection, or pricing decision affects losses, profitability, and capital adequacy. Errors can lead to claims losses, defaults, or regulatory scrutiny, making accountability a core part of the role. - Working under strict regulations and internal policies

Underwriters must follow detailed guidelines and evolving regulatory requirements. Balancing business objectives with compliance obligations requires consistency, documentation discipline, and awareness of policy changes. - Decision-making with incomplete or imperfect information

Not all cases present clear data. Underwriters often make decisions with gaps, assumptions, or time constraints, requiring balanced judgement rather than rule-based thinking alone. - Managing pressure from business and sales teams

Underwriters regularly face pressure to approve cases faster or relax conditions. Maintaining independence while supporting business growth is a key professional challenge. - Handling complex and exceptional cases

As careers progress, underwriters handle higher-value, non-standard, or customised cases. These require deeper analysis, collaboration with risk and legal teams, and stronger justification. - Maintaining ethical standards

Underwriters act as fiduciaries for their institutions. Ethical decision-making, avoidance of conflicts of interest, and fair treatment of applicants are central responsibilities. - Keeping up with changing risk environments

Economic cycles, regulatory updates, climate risks, and technological shifts constantly change risk profiles. Continuous learning is necessary to remain effective and relevant.

Is Underwriting a Good Career Choice in 2026?

Underwriting is a strong career choice in 2026 for professionals who enjoy analytical work, structured decision-making, and accountability. It is a role that stays relevant across economic cycles because every financial institution needs a mechanism to evaluate risk and protect its balance sheet. As insurance markets expand, credit demand grows, and regulations become stricter, underwriting continues to remain a core hiring area across insurers, banks, NBFCs, and fintech lenders.

This career is especially suitable if you are comfortable working with numbers, documents, and policies, and if you can make balanced decisions without being influenced by pressure. It offers clear progression from junior support roles to independent underwriting, then to specialisation and leadership. Compensation improves significantly with domain expertise and experience, particularly in commercial insurance, corporate credit, and complex underwriting segments.

However, underwriting is not ideal if you prefer creative work with low responsibility or if you find repetitive documentation frustrating. Success requires discipline, patience, and a willingness to learn continuously as risk environments and tools evolve. If you want a stable finance-adjacent career with strong long-term demand and a clear growth path, underwriting is one of the better options in 2026.

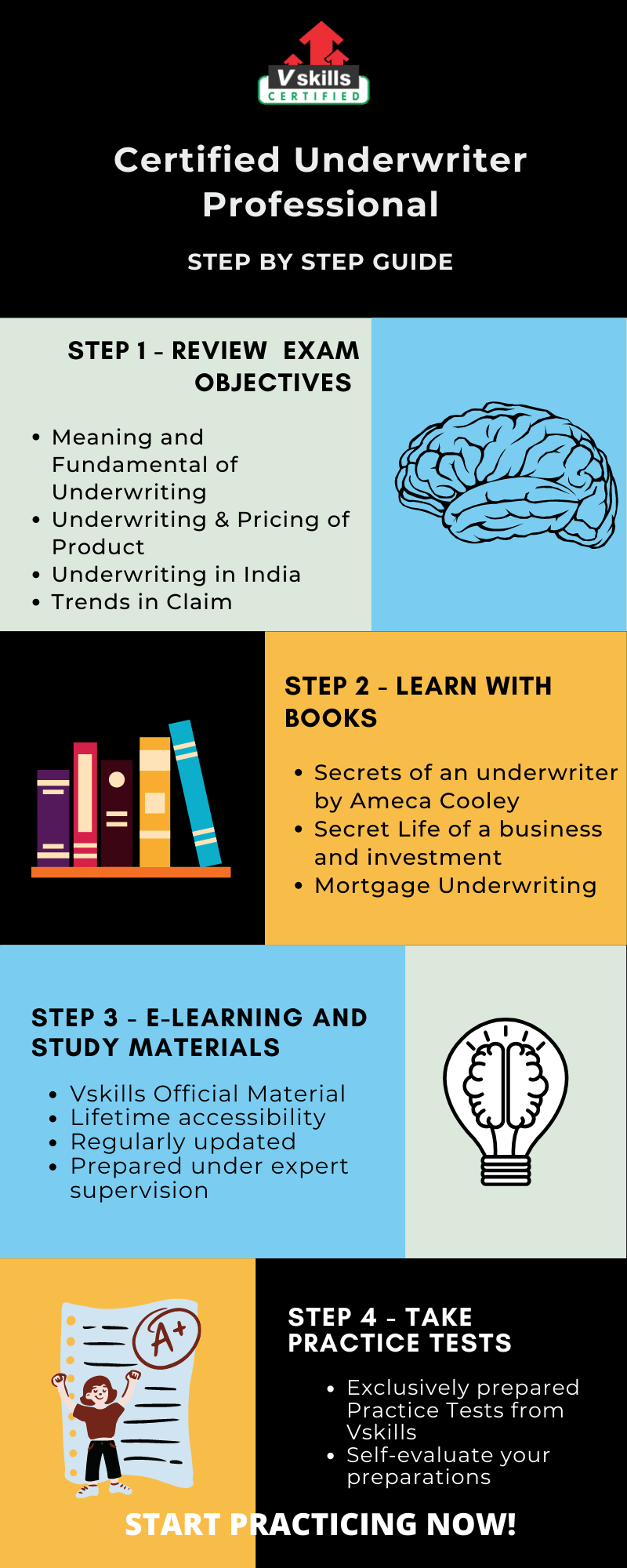

Preparation Guide to become a Certified Underwriter

The best methods to prepare for the Underwriter job roles are by developing a comprehensive strategy that should be implemented before beginning your journey. We have prepared a study guide consisting of all the required study resources and the essential steps for your plan of action before taking the exam.

Step 1 – Review the Exam Objectives

Reviewing every exam objective becomes the most important part of your preparation. Devote enough time to each topic and have in-depth knowledge of the subject. Moreover, this will also result in strengthening your preparation. This certification exam covers the following topics:

- Meaning and Fundamental of Underwriting

- Underwriting & Pricing of Product

- Underwriting in India

- Trends in Claim

Refer: Certified Underwriter Brochure

Step 2 – Learning with Books

Books are meant to improve our memory; they are a traditional source of learning. Although many of us feel that it is a tedious process and a waste of time sometimes, the fact is contrary to such a mindset. Books are beneficial in terms of making you aware of the topics in detail, hence gain command of the required skills.

The books mentioned below are the best books for the Underwriter certification exam.

- Secrets of an Underwriter by Ameca Cooley. The book essentially explores topics like how to approve a loan, how it is evaluated, and what the factors are in underwriting.

- Secret Life of a business and investment. The book consists of all the secrets of the underwriter experience. How to create more business and investment. It has highlighted the major topics in the book

- Mortgage Underwriting. The book explains the domain of the underwriter. It reveals all the principal of the topic and what the outcome of it.

Step 3 – E-Learning and Study Materials

E-learning resources are accessible anytime and anywhere, along with accommodating all educational needs as well. Through E-learning, the lectures can be repeated as per your convenience. Vskills offers E-Learning Study Material for the Certified Underwriter exam. One very special advantage of Vskills learning material is its timely updates and lifetime access. In addition to supporting your e-learning, Vskills also provides study materials in hard copy for candidates preferring offline study methods.

Refer: Certified Underwriter Sample Chapter

Step 4 – Check your Progress with Practice Tests

There is a quote which states that “the more you are accustomed to sitting for a period of time, answering test questions and pacing yourself, the more comfortable you will feel when you actually sit down to take the test”. Practice tests can help us ensure our preparation and familiarize ourselves with the concepts better. So Start practicing with free Practice Tests Now!

Job Interview Questions

Prepare for your next job Interview with Vskills. Latest online Interview questions, these questions are created by experts to help you to overcome the interview fear.

Expert Corner

Becoming an underwriter in 2026 is a practical and high-potential career move if you want a role that combines finance, risk, and structured decision-making. The pathway is clear: build strong fundamentals, enter through an analyst or support role, learn underwriting guidelines and compliance, and then grow through experience and specialisation. As insurance, lending, and capital markets expand, organisations will continue to need professionals who can assess risk accurately and make consistent decisions.

If you approach underwriting with patience and discipline, it can offer long-term stability, strong career progression, and opportunities across multiple industries. The most important step is to start in a role that brings you close to underwriting files and decisions, because that real-case exposure is what turns theoretical knowledge into underwriting judgement.

Strengthen your prospective career benefits by becoming a Certified Underwriter Professional. Start Practicing Now