Hedge funds play a valuable arbitrage role in reducing or eliminating mispricing in financial markets. They are an important source of liquidity, both in periods of calm and stress, and they add depth and breadth to our capital markets. By taking risks that would otherwise have remained on the balance sheets of other financial institutions, they provide an important source of risk transfer and diversification.

These funds perform these functions as they are a critical part of what makes the financial markets work relatively well in absorbing shocks and in allocating savings to their highest return. Hedge funds combine the classic mix of factors that have been associated with institutions at the centre of past instances of stress in financial markets. They can be highly leveraged and can be vulnerable to pressure to liquidate assets quickly if they sustain significant losses. They can be active in complex instruments, and assessing the risks in their exposures is formidably challenging. Additionally, they are not subject to the public disclosure or regulatory reporting requirements that apply to a range of other financial institutions. And they operate largely outside the framework of other requirements established by regulatory authorities to protect the stability of the financial system.

For policy makers, the concerns associated with hedge funds range from investor protection, to market practices and potential manipulation, to the potential conflicts and reputational risks they present to the financial institutions they transact with, and to potential risks to the stability of the financial system. I want to focus on the latter set of concerns – those associated with systemic risk.

These systemic concerns have two dimensions.

- First is the possibility that the behaviour of hedge funds in periods of market stress could amplify rather than mitigate the shock, induce larger moves in asset prices, or cause broader damage to the functioning of markets when it is most important they function well.

- Second is the possibility that the failure of a major hedge fund or group of funds could significantly damage the viability of a major financial institution, both through direct exposure to the fund and losses resulting from the impact on other market risks to which the institution is exposed.

These concerns existed before the events associated with Long-Term Capital Management (LTCM) in 1998, but that episode provided a powerful example of both sets of risks, and how the erosion of counterparty discipline can magnify those risks.

Impact on Economy

On the one hand hedge funds contribute to market liquidity as they tend to be more willing to put their capital at risk in volatile market conditions. Market shocks can hence be more easily absorbed. This also means better possibilities for investors to diversify their portfolio.

Hedge funds also enhance the spreading of risks among market participants. They take risks that otherwise would have remained in the company’s books. As active risk takers they account for the development of sophisticated over-the-counter markets such as the credit derivatives market. This is valuable for the price discovery process.

On the other hand there are also worrying effects. Because of the relatively small funds invested in hedge funds in relation to the total volume of the international financial markets the risks emanating from hedge funds were underestimated initially. Due to the close relation between hedge funds, banks and financial markets, a hedge fund related triggering event associated with either of them may be further escalated through these mutual links. As a consequence of the near collapse of LTCM, hedge funds and banks take into account the interaction between leverage, credit risk and liquidity risk.

Without adequate liquidity reserves a fund could be forced to default on its margin calls. If the situation then is aggravated by asset illiquidity in stressed markets, hedge funds may not be able to unwind their positions at reasonable prises and banks could have difficulties in liquidating collateral. Another risk occurs for markets, banks and counterparties if a hedge fund that is holding a highly concentrated position is facing a lack liquidity or worse. Limited disclosure and thus little transparency is another issue, as regulators may not be aware of the risks outstanding in the market. Investors may not be aware of the exact risk situation of a hedge fund they are investing in.

Hedge funds can also cause excessive market volatility due to the short-term-oriented strategies that they follow. Volatility can also be enhanced because hedge funds by their financial power are able to influence asset prices and thus make other market participants change their behaviour in a way market dynamics work in favour of the fund.

If hedge funds attempt to exploit profitable opportunities from similar strategies the positioning of individual hedge funds can become more similar. If the hedge funds also react similarly towards events, the unwinding of leveraged positions could be disruptive. Exposures to hedge funds represent a great source of risk to a bank because of the complexities associated with the management of such exposures. No matter if they are direct exposure like financing, trading and investing or indirect as exposures to counterparties that have exposures to hedge funds.

Another issue is the potential risk for insider trading. Funds that deliberately go short or long in individual shares are a possible risk factor. They frequently trade these specific shares and it is plausible that they will have a relatively large share in the total volume of transactions. HF managers will go very far to acquire information about the company’s policy.

Impact on Investors

Professional investors

As hedge funds are neither publicly sold nor advertised, new investors are generally attracted through the word of mouth, consultants, registered representatives, brokers or investment advisors. High net worth individuals have been the dominant source of funds for hedge funds.

For individual investors most hedge funds have minimum investment requirements as well as lock-up periods which require a certain knowledge and financial flexibility and only allowed few individuals to invest. Growing knowledge concerning hedge fund products and their risk adjusted diversification properties has also motivated demand from institutional investors. Low interest rates contributed to this evolution as well.

Pension funds, endowments as well as insurance companies were interested in high returns. Generally insurance companies look for rather safe places to put their money in order to stay solvent. They utilize the HF investment of a small amount of their funds to amplify the return of their total investment.

Private investors

Over time hedge funds have become far more available to a greater number of private investors who cannot be regarded as financially experienced nor as owning large funds who could easily bear losses from speculation. News about tremendous benefits in the past caused a rising demand from the broader public.

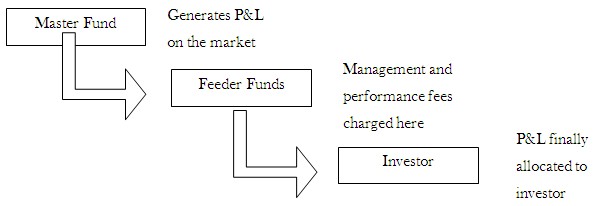

While this growth provides hedge funds with new investors and investors with new possibilities of returns, this also raises serious concerns. For these investors it is difficult for them to measure the performance of a hedge fund. Traditional funds for example, take positions relative to a benchmark. After a certain period the risk adjusted returns are compared with a relevant index. This determines whether the manager performed well or not. On the contrary when one has to measure the performance of a hedge fund, the first problem relates to their aim for absolute returns. The huge discretion in choosing the investment strategy makes it difficult to quantify the risk in advance. Also, there is little or no data on which to base the assessment.

The second problem faced is that, published historical returns of hedge funds are not necessarily reliable data as it is often based on voluntary contributions by fund managers. Furthermore published returns are gross returns. Investors usually receive net returns after a deduction of costs and management fees.

The results provided by the hedge fund do not allow insight into the investment strategy pursued either. Complications may arise when adjustments have to be made for additional deposits/withdrawals, reorganizing within portfolios, dividend payments or index payments.

Limited marketability is another drawback with hedge funds as they are not listed and publicly priced and due to lock-up periods an investment cannot easily be sold. Market impact and the risks make investing into hedge funds highly complex. Complex and to a certain extend dangerous products mean a challenge for a serious selling.

As a second issue the limited financial knowledge and usually few experience of a private investor has to be taken into account. This requires a kind of distribution that is both adapted to the very special nature of the product and matching the needs of advice of the investor.

In the absence of sound product information for the customer everything is left to the advisor consulted by the investor. But managers are said to lack sufficient knowledge of the underlying investments and do not always fully understand the consequences of their investment policy. This does not only raise questions about the quality of a fund’s management but as well causes concerns about any serious distribution of hedge funds investment to a broader public.

The sale of hedge funds is currently market adapted to the needs and demands of very wealthy individuals and professional investors who both do not suffer from financial losses in the same way as the broad public would. The complexity of the product as such does not match the limited financial knowledge and need for advice of an ordinary retail investor.

The hedge fund industry plays more of a role in creating liquidity and making markets efficient than the mutual fund industry. The hedge fund industry can do so because it is generally not regulated, so that funds are free to take whatever positions they wanted and to make full use of financial innovations. As the hedge fund industry grows, regulation becomes more likely, and large hedge funds are likely to become more similar to financial institutions.

Apply for Hedge Fund Certification!

https://www.vskills.in/certification/certified-hedge-fund-manager