It is the most widely used business performance measurement framework, introduced by Robert S. Kaplan and David P. Norton in 1992. Balanced scorecards were initially focused on finding a way to report on leading indicators of a business’s health, they were refocused to measure the firm’s strategy that directly relate to the firm’s strategy. Usually the balanced scorecard is broken down into four sections, called perspectives, as

- The financial perspective – The strategy for growth, profitability and risk from the shareholder’s perspective. It focuses on the ability to provide financial profitability and stability for private organizations or cost-efficiency/effectiveness for public organizations.

- The customer perspective – The strategy for creating value and differentiation from the perspective of the customer. It focuses on the ability to provide quality goods and services, delivery effectiveness, and customer satisfaction

- The internal business perspective – The strategic priorities for various business processes that create customer and shareholder satisfaction. It aims for internal processes that lead to “financial” goals

- The learning and growth perspective – The priorities to create a climate that supports organizational change, innovation and growth. It targets the ability of employees, technology tools and effects of change to support organizational goals.

The Balanced Scorecard is needed due to various factors, as

- Focus on traditional financial accounting measures such as ROA, ROE, EPS gives misleading signals to executives with regards to quality and innovation. It is important to look at the means used to achieve outcomes such as ROA, not just focus on the outcomes themselves.

- Executive performance needs to be judged on success at meeting a mix of both financial and non-financial measures to effectively operate a business.

- Some non-financial measures are drivers of financial outcome measures which give managers more control to take corrective actions quickly.

- Too many measures, such as hundreds of possible cost accounting index measures, can confuse and distract an executive from focusing on important strategic priorities. The balanced scorecard disciplines an executive to focus on several important measures that drive the strategy.

The scorecard approach keeps the company’s vision, mission, and goals centric. Additionally, it considers the four different perspectives of financial, customer, internal business process, and learning and growth to assess performance. All perspectives impact how the organization is doing.

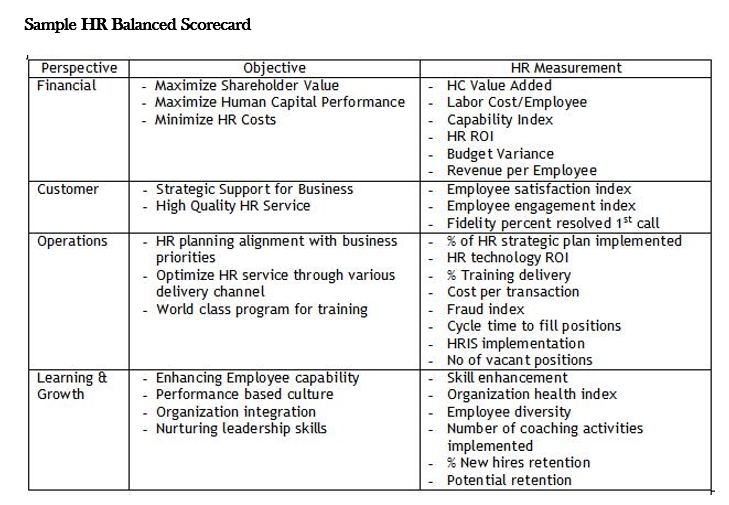

HR Balanced Scorecard

Similar to balanced scorecard (BSC) as above, HR department scorecard involves perspectives

- Financial

- Internal

- Customer

- Learning / Growth

Internal Business or Strategic Perspective

Since the basis for the HR Balanced Scorecard is achieving business goals, the aligned HR Strategic objectives are the drivers for the entire model.

“How do our internal processes function to efficiently deliver products and services, and how can we improve our efficiency?”

It can be implemented as

- Metric: Servicing customer calls in our call center.

- Target 1: Answer each incoming phone call from a customer within one minute.

- Target 2: Decrease the number of dropped calls to less than 2%.

- Method: This metric will measure the elapsed time from the moment when incoming phone call reaches our network to the time it is picked up by an operator. An automated phone auditing IT system will be implemented to track phone statistics.

Learning and growth or Operations Perspective

The focus was primarily in three areas: staffing, technology, and HR processes and transactions.

“How well are we positioned to ensure that goals are met in the future?”

It can be implemented as

- Metric: Staff development.

- Target: Each employee has to take training ABC by the end of March next year and succeed at least 80% score on a test.

- Method: The company will offer training ABC that will be followed by a test.

Customer Perspective

Includes measures of how HR is viewed by the key customer segments. Survey results were used to track customer perceptions of service as well as assess overall employee engagement, competitive capability, and links to productivity.

“How well are we meeting the needs of our customers, and how can we make them more satisfied?”

It can be implemented as

- Metric: Overall satisfaction ratings measured via surveys and polls.

- Target: At least 4.00 out of 5.0 from each of the major customer groups: youth, adult, elderly.

- Method: A final question in each survey asks the respondent to rate his or her overall satisfaction. Data for this metric is compiled monthly.

Financial Perspective

Addresses how HR adds measurable financial value to the organisation, including measures of ROI in training, technology, staffing, risk management, and cost of service delivery

“How well are our finances managed to achieve our mission?”

It can be implemented as

- Metric: The Sales department expenditures as a proportion of company expenditures.

- Target 1: The Sales department expenditures will be less than 20% of the total company expenditures.

- Target 2: The Sales department expenditures will grow at the same or lower rate than revenues from sales.

- Method: Total expenditures of company and revenues from sales figures will be obtained from the corporate accounting system. Expenditures for the Sales department will be obtained from intradepartmental book-keeping system. These two figures will be used to calculate the percent.