Pillar 1 describes the rules to calculate and report the minimum regulatory capital standards for credit, market and operational risk. Compared to the 1998 Capital Accord, the new requirements aim to better align economic and regulatory capital requirements; reducing incentives for regulatory arbitrage.

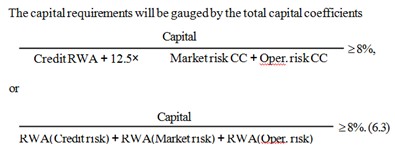

The capital coefficient must amount to at least 8%. The innovations of the new capital accord relate mainly to improvements in the risk measurement, i.e. in the computation of the denominator.

The Standardized Approach

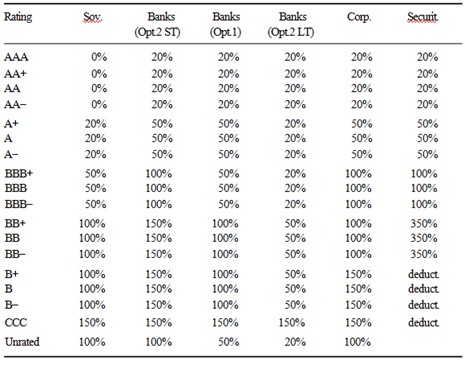

The standardized approach is a further sophistication of the Basel I Capital Accord with a more specific classification of the credit risk. The measurement of the credit quality is determined by an External Credit Assessment Institution (ECAI). The risk weights for the standardized approach for the different asset classes are summarized in the table below. Using the external ratings, it is seen that the risk weights are more sensitive to the risk than before, where, e.g., a flat 100% risk weight for firm exposures was applicable.

Regulatory risk weights (SA)

The risk weights for the various asset classes are described in the section below. For banks that do not have the intention to spend a lot of resources to the Basel II implementation, Appendix 9 of table provides an overview of the simplest options in the standardized approach.

Sovereigns and central banks The Basel I Capital Accord assigns a zero risk weight to OECD member countries. Non-member countries received a risk weight of 100%. In the Basel II Capital Accord, the rating depends upon the ECAI rating. The highest ratings (AAA to AA-) receive a zero risk weight, the lowest ratings (CCC and lower) a risk weight of 150%. The risk weights are assigned to rating categories as can be seen from the above table. In addition to ECAI ratings, supervisors may recognize the country risk scores of export credit agencies (ECAs) that follow the OECD methodology. Scores 0 to 1, 2, 3, 4 to 6 and 7 correspond to rating zones AAA to AA-, A+ to A-, BBB+ to BBB-, BB+ to B- and CCC, respectively.

Central banks and other international institutions follow the same scheme. Some international organizations and multilateral development banks that comply with the BCBS criteria receive a zero risk weight, like the Inter- national Monetary Fund, the Bank for International Settlements, the World Bank and the European Commission. The risk weight is evaluated on a case-by-case basis and is reviewed regularly.

Table: Risk Weights in the standardized approach for Basel II

Exposures of banks to their sovereign of incorporation denoted in local currency may be assigned a lower risk weight. The same risk weight can be decided by other national supervisors for claims of their banks concerning domestic currency claims to that sovereign.

Non-central government public sector entities follow the approach for banks without the preferential treatment for short-term claims. Certain domestic public sector entities may be treated as sovereigns, in whose jurisdiction the public-sector entities are established. This choice is subject to national discretion.

Banks that are incorporated in an OECD member country received a risk weight of 20% in the Basel I Capital Accord. Other banks received a risk weight of 100%. Under Basel II, national supervisors can choose between two options. Under option 1, claims on a bank are assigned a risk weight one category less favorable than that of the sovereign of its domiciliation (Table above).

The risk weight depends on the rating of the sovereign, not of the bank. Under option 2, a bank receives the risk weight corresponding to its external credit assessment for long-term (LT) positions. Low-risk and short-term (ST) positions with an original maturity less than 3 months receive a lower risk weight. An unrated bank cannot receive a risk weight lower than applied to the sovereign.

Claims on securities firms receive the risk weight of banks when these firms are subject to a similar regulatory framework. Otherwise, securities firms follow the risk weight for firms.

Firms Firm claims were assigned a risk weight of 100% independent of the credit quality in Basel I. Basel II assigns a risk weight to firms (including insurance companies) that depends upon the rating. The risk weight ranges from 20% to 150% as reported in the table above. The risk weight for a firm cannot be lower than the risk weight of the sovereign of incorporation.

Retail Retail exposures are subject to a lower risk weight of

RW(retail) = 75%.

Retail exposures are exposures to individual persons or small businesses. The concerned products are revolving credits, lines of credit (e.g., credit cards and overdrafts), personal term loans and leases (e.g., installment loans and leases, student and educational loans, personal finance). The facilities in a retail portfolio need to be sufficiently granular, e.g., a counterpart’s exposure in the retail portfolio may not exceed 0.2% of the total portfolio and may not exceed d1 million.

The risk weight of 75% is beneficial for small companies with respect to large companies. It stimulates the economic framework of small and medium-sized enterprises (SMEs). Local regulators can increase the risk weight when the local loss statistics indicate higher risk. A risk weight of 100% is applicable under Basel I.

Claims fully secured by mortgages or residential property that is or will be occupied by the borrower, or that is rented, will be risk weighted at

RW(residential mortgage) = 35%.

The risk weight is only applicable for residential purposes and when the claim is sufficiently secured. When the local loss statistics indicate that a higher risk weight is required, local regulators may require banks to increase the risk weight accordingly in their jurisdiction. In the Basel I framework, a risk weight of 50% was assigned to these facilities.

Claims secured by commercial real estate receive a risk weight of 100%. The BCBS justifies the high risk weight because these exposures have been a recurring cause of troubled assets in the past few decades. Well-defined exceptions allow local supervisors to lower the risk weight to 50% in well-developed and long-established markets. In conclusion, one has

RW(commercial mortgage) = 50% or 100%.

In Basel I, the risk weight is equal to 100% as well, except for specific extinct cases where 50% is applicable. Note that the risk weights for residential and commercial real estate allow physical collateral to be taken into account.

The above risk weights are applicable for all loans except for past due loans that receive a higher risk weight.

Securitization

For securitization purposes, the risk weights are assigned towards long-term or short-term ratings. From the Risk Weights Table above, it is seen that the risk weight becomes very high for low-rated tranches. For the lowest ratings, a deduction from capital is required, where the general rule is to deduct 50% of the Tier 1 and 50% of the Tier 2 capital. For off-balance sheet exposures, a credit conversion factor is applied and the corresponding risk weight is applied.

Past due loans and higher-risk categories Specific weights are applicable under Basel II for loans past due more than 90 days. The unsecured portion of such loans, net of specific provisions, is weighted with RW(past due) = 100% or 150%, depending on the amount of specific provisions (above or below 20%), and the supervisory regulation. In the case of qualifying residential mortgage loans, the risk weight is 100%.

The Basel II Capital Accord explicitly recognizes higher risk categories to which a higher risk weight is assigned: claims on sovereigns, public sector entities, banks and securities firms with a rating below B-; claims on firms rated below BB-; past due loans mentioned above. Securitization tranches rated between BB+ and BB- are risk weighted at 350%. National supervisors have the discretion to define higher risk weights for other assets like, e.g., venture capital and private equity investments.

Other Assets

The treatment of other assets is subject to a general risk weight of

RW(other assets) = 100% or 150%.

Investments in equity or regulatory capital instruments issued by banks or securities firms will be risk weighted at 100% unless deducted from capital.

Unrated Facilities

The risk weight for unrated counterparts/facilities reflects the average risk for that type of counterpart world- wide. It assumes that there is no systematic adverse selection that unrated counterparts are weaker. National supervisors sometimes increase the risk weight for unrated counterparts to put the risk weight in line with the local risk experience.

Off-balance sheet items

Off-balance sheet items are converted to an equivalent credit exposure via the credit conversion factor (CCF): equivalent credit exposure = CCF × off-balance sheet exposure.

The following CCF values apply:

- CCF = 0%: Commitments that are unconditionally, at all time and without prior notice cancellable or when the cancellation results from a deterioration of the borrower’s creditworthiness.

- CCF = 20%: Commitments with an original maturity up to one year; short-term self-liquidating trade letters arising from the movement of goods.

- CCF = 50%: Commitments with an original maturity over one year (long-term commitments).

- CCF = 100%: Lending of bank’s securities or the posting of securities as collateral by banks.

For a commitment on an off-balance sheet item itself, the lowest of the two CCF values is applied. Consider for example an unconditionally cancellable commitment (CCF = 0%), for example on a commitment of a bank to a short-term trade letter (CCF = 20%): for this type of “double” commitment, one applies the lowest CCF of 0%. In the case of a long-term commitment on a long-term commitment, the CCF is equal to 50% and not equal to 50% × 50% = 25% that would be obtained by multiplying the CCF values.

Banks are encouraged to develop systems to track and monitor credit risk exposures arising from unsettled and failed transactions. One considers two types of products:

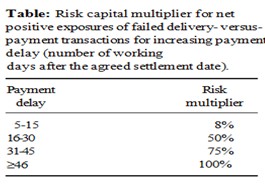

Delivery-versus-payment: For transactions settled trough delivery-versus-payment (DvP) or payment-versus-payment (PvP) systems, the exposure is the difference between the agreed settlement price and the current market price, i.e. the positive current exposure. The capital charge is obtained by multiplying the positive current exposure by the capital multipliers of the following table:

Free-delivery: For non-DvP or free-delivery transactions, where cash is paid without receipt of the corresponding receivable (securities, foreign currencies, gold, or commodities), the exposure amount is the full amount of cash paid or value-delivered deliverables. The risk weight depends on the payment or delivery delay:

- If the other part (so-called second leg) of the transaction is not received at the end of the business day, the exposure is treated as a loan either in the standardized or IRB approach.

- If exposures are not material, a uniform risk weight of 100% may be applied.

- If the second leg is not received after 5 business days of the payment or delivery date, the exposure and possible replacement costs are deducted from capital.

The risk weight or deduction remains applicable until the actual delivery or payment.

Implementation aspects (SA)

The use of ratings for capital charges implies various application issues. Many of these issues concern the practical interpretation and use of different ratings.

Split ratings

In the case of multiple assessments, split ratings can occur. One uses the most conservative risk weight in the case of two external ratings. When there are more than two external ratings, one selects the highest of the two lowest risk weights. For example, a firm with ratings AA-, A, BBB+ and BBB, is assigned the risk weight 50% corresponding to the rating A. Banks must disclose the used ECAIs and use all available ratings to avoid cherry-picking. These rules result in the moderately conservative risk weights in the case of split ratings.

Mapping process

There exist multiple rating agencies in the world of which not all adopt the AAA, AA+ etc., rating scale. Supervisors need to determine the eligible ECAIs for the standardized approach. Furthermore, they also need to map their ratings to the corresponding risk weights, e.g., based upon past default and loss statistics.

Local and foreign currency ratings

Foreign currency ratings are applied for foreign currency exposures. For local currency exposures, local currency ratings are applied. When the transfer risk is sufficiently mitigated, local currency ratings can also be applied to foreign currency exposures.

Issue and issuer ratings

The risk weight is assigned based upon the issue-specific rating. It can occur that the bank invests in an unrated issue, while other issues or the issuer itself are rated. When the bank invests in a facility that is more senior or equal ranks with the rated issue, this rating can be used; otherwise the bank’s issue is unrated.

The issuer rating is considered to apply for senior unsecured claims, and can only be applied to assign risk weights to issues equally or higher rated. For senior secured exposures where the seniority is already taken into account in the issue rating, the risk mitigant cannot be taken into account twice. The improved rating cannot be used to apply a lower risk weight and at the same time apply a risk mitigant to further reduce this lower risk weight.

Group and holding ratings

Ratings assigned to a group or to an entity cannot be applied to other entities within the same group, although this would reduce the number of unrated issues.

Short-term ratings

Short-term issue ratings are applicable to banks and firm exposures. Short-term ratings A-1/P-1, A-2/P-2 and A-3/P-3 correspond to risk weights of 20%, 50% and 100%, respectively. The rules for short-term exposures are further detailed in.

Unsolicited ratings

To avoid ECAIs putting pressure on issuers, banks should only use solicited ratings. When such unwanted behaviour of an ECAI is identified, national supervisors should reconsider its eligibility.

Risk mitigation (SA)

Collateralized transactions

In a collateralized transaction, the (potential) credit exposure is hedged in whole or in part by collateral posted by a counterpart or by a third party on behalf of the counterpart. The collateral is taken into account via the comprehensive approach or via the simple approach. Banks can choose either one of both approaches for the banking book. For the trading book, only the comprehensive approach can be applied.

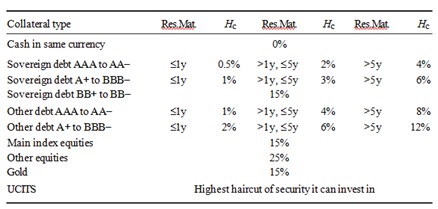

Several conditions have to be satisfied to make the collateral eligible for risk weight reduction. For the simple approach, the eligible collateral types are specified. These collateral types are called financial collateral and are also eligible under the internal ratings based approach. Among others, one finds cash, deposits, gold, debt securities, equities included in a main index, Undertakings for Collective Investments in Transferable Securities (UCITS) and mutual funds.

Debt securities are recognized when they have a sufficiently high rating from an ECAI (e.g., at least BB- for sovereign debt and BBB- for other entities), or when it is issued by a bank and information is available to indicate sufficient quality. For the comprehensive approach, listed equities and UCITS or mutual funds that include such equities are also eligible as collateral.

Legal requirements have to be satisfied to ensure that the bank has the right to liquidate or take legal possession of the pledged collateral in a timely manner after a default event. The collateral may not be correlated materially with the debt value in order to provide sufficient protection. For example, shares of the same counterpart do not provide protection in a default risk event. Collateral assets held by a custodian bank should be segregated from the custodian’s own assets. The impact of collateral is calculated either via the comprehensive or the simple approach.

Comprehensive approach

In the comprehensive approach, the haircut exposure is adjusted with the haircut collateral. The exposure after risk mitigation for a collateralized transaction is calculated as follows:

E = max (0; E × (1 + He) – C × (1 – Hc – Hfx))

= max (0; E – C + He × E + C × Hc + C × Hfx)

The above model can be considered as a white box model. Haircuts take into account the uncertainty of the exposure (He) and the uncertainty of the collateral value at liquidation. There are various reasons why the exposure and collateral value can fluctuate: exchange rate (Hfx) and price market fluctuations (Hc). The exposure haircut increases the current exposure E and the resulting net exposure E at which the risk weight is applied, the other two haircuts reduce the collateral value C and increase the net exposure E. When the collateral consists of a basket of assets, one calculates the amount-weighted average haircut of the asset haircuts and applies it to the basket.

Table: Examples of standardized supervisory collateral haircuts Hc assuming a 10- business day holding period and daily mark-to-market.

Banks can either choose standardized supervisory haircuts or internal estimates of market-price volatility. The haircuts depend on the instrument type, the transaction type, etc. the table below provides some examples of standardized supervisory haircuts assuming a 10-business-day holding period.

Debt securities with ratings lower than indicated in the table are assigned equity haircuts listed on a recognized exchange. The exchange rate haircut takes into account currency risk when exposure and collateral are denominated in different currencies. It is calibrated at Hfx = 8% for a 10-day holding period and a daily mark-to-market.

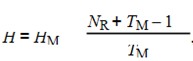

When this is not applicable, a rescaling formula is applied:

with H the resulting haircut, HM the haircut under the minimum holding period, TM the minimum holding period for the transaction type and NR the actual number of business days between remargining for capital market transactions or revaluation for secured transactions. When the regulatory haircuts are applied, one obtains HM from the table above and TM = 10.

Internal estimates are based upon a 99th percentile VaR that is estimated using at least one year of data history. For daily remargining or revaluation, the holding period ranges from 5 to 10 business days depending on the type of facility, and can be adjusted in the case of low liquidity. These resulting haircuts are scaled using the square root law (assuming Brownian motion) adjusting for longer holding periods or less frequent revaluations. When internal haircuts are applied, one needs to update at least every 3 months the datasets and evaluate the resulting haircuts. The VaR haircuts are evaluated using a variety of techniques available for market risk.

In the latter case, the previous equations:

E = max (0; E × (1 + He) – C × (1 – Hc – Hfx))

= max (0; E – C + He × E + C × Hc + C × Hfx)

Becomes:

E = max 0; E-C + VaR(0.99) × multiplier .

When these estimates exhibit too many exceptions, a penalization scaling factor ranging from 1 to 1.33 is applied similar to the internal market risk approach explained below. For netting E becomes

E = max 0; E-C+|Es| × Hs +|Efx| × Hfx,

with |Es| the absolute value of the net position in a given security and |Efx| the absolute value of the net position in a currency different from the settlement currency. Details for repo-style transactions are also provided in [63]. It is also important to remark that under certain circumstances, a zero haircut can be applied.

Simple approach

In the simple approach, the risk weight of the counterpart is substituted by the risk weight of the collateral (subject to a 20% floor) for the collateralized portion of the exposure, similar as in the Basel I accord. The collateral must be pledged at least for the life of the exposure and has to be marked to market and revaluated with a minimum frequency of 6 months. The risk weight floor of 20% can sometimes be reduced to 10% and 0%.

Collateralized OTC derivatives transactions

The counterpart credit risk charge for this type of products is calculated by either the current exposure method, the standardized method, or the internal model method. The latter two are more complex approaches and will be discussed below. Using the current exposure method, the capital requirements are obtained as:

capital = EAD × RW × 8%

EAD = (RC + add-on) – CA,

with RC ³ 0 the positive replacement cost or current exposure, CA the haircut collateral amount, RW the counterpart’s risk weight.

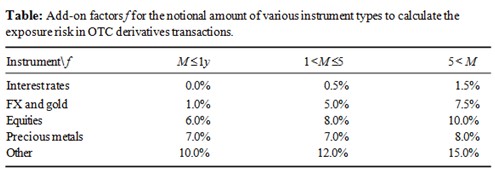

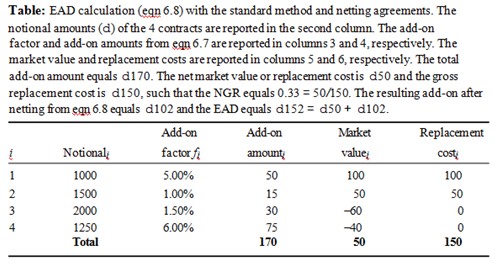

The add-on

add-on i= fi × notional amount i is obtained as the transaction notional times the add-on factor f reported in the table. For an OTC contract on gold with notional of $1000 with a current market value of d40 and remaining maturity of 20 months, the EAD is calculated as EAD = 40 + 5.0% × 1000 = 90

If the counterpart is an externally rated bank with an A+ rating, the risk weight is 50% and the risk weighted assets for this transaction are d45 (= 50% × d90). Also, for the total return swaps and credit default swaps in the trading book, this methodology is applicable with add-on factors equal to 5% or 10%. The 5% is applicable when the underlying is a qualifying reference obligation otherwise the 10% add-on factor is applied. In the case of legally enforceable netting agreements, the replacement cost is the net replacement cost (floored at zero) corrected by collateral with haircut adjustments. The portfolio add-on is calculated as

add-on = (0.4 + 0.6NGR) i,

add-on i,

Where, the NGR is the ratio of the current net replacement cost with respect to the current gross replacement cost (without netting). Via the NGR, the current netting benefits are passed to future exposure risk. The method is illustrated in the table below:

On-balance sheet netting

Banks may have loans and deposits of the same counterpart. When the bank has legally enforceable netting arrangements in the concerned jurisdictions, the bank may calculate the capital requirement for the net exposure. The legal framework should hold in the case of default and bankruptcy procedures. It is also important that the bank has sufficient monitoring and controls. In the case of currency mismatches, one applies haircuts as in the case of collateral following the same approach.

Guarantees and credit derivatives

Guarantees and credit derivatives provide protection against credit losses. When there are legal requirements fulfilled such that the protection is direct, explicit, irrevocable and unconditional, and when supervisors are satisfied with the banks operational conditions, such risk mitigants may be taken into account for the capital requirements. Additional requirements concern explicit documentation of the guarantee and the timing and conditions when the bank can pursue the guarantor.

Because credit derivatives are complex products, there are many additional requirements concerning the definition of the credit event, identity of protection sellers, mismatches of maturity (including grace periods) and the underlying obligation of the credit derivative and the reference obligation in the bank’s portfolio.

The range of eligible guarantors or protection sellers includes sovereigns, public-sector entities, banks and securities firms that have a lower risk weight than the counterpart for whom protection is given. Other entities are also required to have a rating higher or equal to A-. A good-rated parent company can give guarantees to weaker subsidiaries. The risk weight of the protected part becomes the risk weight of the guarantor or protection seller. The uncovered portion is weighted based upon the underlying counterpart. Haircuts are applicable in the case of currency mismatches.

Maturity mismatches

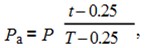

A maturity mismatch exists when the residual maturity of the risk mitigant or hedge is less than the maturity of the underlying exposure (including grace periods). A hedge with maturity is only recognized as a credit risk mitigant when the original maturity is at least one year. In the case of a maturity mismatch, one applies the following formula:

Where, Pa is the adjusted value of the protection for the maturity mismatch; P is the value of the

credit protection; t is the minimum of the T and the remaining maturity of the credit protection and where T is the remaining maturity of the exposure capped at 5 years.

Maturity is also capped at 5 years in the internal ratings based approach; which will be discussed after the examples in the next section.

Examples: We illustrate the exchange rate risk haircut and the collateral haircuts by some examples

- Consider an exposure of d100 that is backed by collateral of d60 of AA long-term debt with a remaining maturity of 8 years. The net exposure is equal to

E = 100 – 60 × (100% – 8%) = 44.8,

Where, the 8% haircut for long-term other debt with AAA-AA rating is applied. In the case of a sovereign security, the haircut is equal to 4% and the net exposure would be equal to 42.4.

- Consider an exposure of d100 that is backed by collateral of US$50 of A-rated medium-term debt with a remaining maturity of 4 years. The net exposure is equal to:

E = 100 – 50 × (100% – 6% – 8%) = 57.

The 6% haircut takes into account the risk of the collateral; the 8% haircut takes into account the exchange rate risk. In the case of a 20-day holding period, the 6% haircut is multiplied by root (20/10) and becomes 8.5% and the net exposure 58.2. When the revaluation is done weekly instead of daily, one multiplies by root (24/10), taking 10 + 4 additional days in the numerator for the 10 more days in the holding period and the 4 more days for the revaluation.

Consider an exposure of d1000 subject to a risk weight of 100% with a remaining maturity of 3.5 years. The full exposure is guaranteed by an entity with 20% risk weight for the first 2 years. The maturity mismatch results in the adjusted protection

The not protected part is equal to 1000-538.5 = 461.5. The resulting risk weighted assets are equal to

RWA = 538.5 × 20% + 461.5 × 100% = 569.2.

In the case of no maturity mismatch, the risk weighted assets would be equal to 200.

The Internal Ratings Based (IRB) Approach

In the internal-ratings-based approach (IRBA), the risk weighted assets (RWA) are for most asset classes obtained as a function of the risk components

RWA = f (PD, LGD, EAD, M).

The function f has been specified and may vary across different asset classes. For some specific, high-risk assets, lookup tables with risk weights are still applied.

Specific to the internal-ratings-based approach is that the risk weights and regulatory capital requirements are (partially) calculated based upon the bank’s internal measurements of the risk components.

The internal measurements need to comply with regulatory standards. Internal estimates of the credit risk parameters for default risk, loss risk, exposure and maturity are allowed depending on the chosen approach:

- IRBAf: In the foundation internal-rating-based approach (IRBAf), the internal estimate for the probability of default (PD) is used to calculate the capital charge, while the other parameters are supplied by the regulator.

- IRBAa: In the advanced internal-ratings-based approach (IRBAa), banks are allowed to provide internal estimates for LGD, EAD and maturity. Because the Basel II risk weight formulae do not use an asymptotic single risk factor model for the LGD, the LGD entered in the risk weight formula is a stressed default-weighted LGD, averaged over all defaults.

Probability of default (PD): The PD for firm, bank and sovereign exposures is not lower than the 5-year averaged one-year default rate. The concerned default rate is the observation weighted default rate. For firm and bank exposures, a floor of 0.03% is applicable. The PD of the default grades is equal to 100%.

The PD measures the risk of the borrower default. Separate exposures to the same borrower must be assigned the same86 borrower default risk grade. The PD estimate must be a long-term average of one-year default rates for the specific grade.

The options to estimate the default risk are the estimation based upon internal default experience, the mapping to external data, and statistical default models. One method can be used as the main approach and another can be used for benchmarking. The minimum data history needs to be at least 5 years for one data source. The use of longer data histories is recommended where possible. The lower the number of observations, the higher is the uncertainty on the PD estimate and the more conservative the calibration must be.

Loss given default: (LGD) reflects transaction-specific factors such as collateral, seniority, product type, etc. In the foundation IRB approach, one can assign transaction-specific risk implicitly via an expected loss dimension or via an LGD dimension. In the advanced IRB approach the LGD dimension is the only option.

The IRBA methodology depends upon three key factors:

- Risk weight functions: The risk weights and risk weighted assets are computed from risk weight functions.

- Risk components: The risk components used in these risk weight functions (PD, LGD, EAD, p, M) are internal risk parameter estimates of which some are supervisory estimates. The asset correlation parameter p is set by the regulator.

- Minimum requirements: The risk weight functions and internal risk parameter estimates can be used on condition that banks comply with minimum standards such as the Basel II default definition.

A firm exposure is defined as a debt obligation of a corporation, partnership or proprietorship. Small and medium-size firms are assigned an up to 4% lower correlation than large firms. The firm asset class also includes insurance companies.

The firm asset class also contains 5 firm asset classes that are defined specifically for specialized lending transactions. In specialized lending, the exposure is typically a special purpose entity that was created specifically to finance or operate financial assets and where it has little or no other material assets or activities.

The primary source of income for repayment is generated by the assets of the special purpose entity rather than a broader commercial organization. In most situations, the bank is a close partner of the specialized lending transaction and has a substantial control on the assets and the generated income.

The 5 subclasses for specialized lending are:

- Project finance (PF): The revenues are typically generated by a single large and complex project, e.g., power plants, chemical plants, mines, tunnels, bridges, or other infrastructure projects and telecommunications infrastructure.

- Object finance (OF): The transaction has the aim to acquire a large physical asset, e.g., ships, aircrafts, satellites. The repayment of the claims depends on the cash flow generated by the object.

- Commodities finance (CF): Structured short-term lending to finance reserves, inventories or receivables of exchange-traded commodities like crude oil, metals or crops. The debt is repaid by the proceeds of the sale of the commodities.

- Income-producing real estate (IPRE): The debt is used to fund real estate like office buildings to let, retail space, multifamily residential buildings, industrial or warehouse space, or hotels. The primary source of cash flows to repay the debt are lease payments, rental payments or the sale of the real estate asset.

- High-volatility commercial real estate (HVCRE): The financing of some real estate types is more risky that IPRE transactions. Such transactions are categorized by the national supervisors based upon the volatility and correlation of past loss history and may include land acquisition, development and construction, as well as transactions where the source of the cash flows is sufficiently uncertain.

A Categorization of exposures into asset classes (IRBA)

There are 3 regulatory asset classes defined:

- Sovereign exposures: This asset class covers all the exposures defined as sovereigns in the standardized approach. It also includes national banks, certain multilateral development banks, international organizations, as well as some types of public-sector entities.

- Bank exposures: As in the standardized approach, the bank asset class covers banks and certain securities firms that are subject to regulation. It also contains multilateral development banks and public-sector entities that are not categorized as sovereigns.

- Retail exposures: An exposure is a retail exposure when it meets a long list of criteria defined. These criteria concern the nature of the borrower or the low value of the individual exposures and the large number of exposures. Exposures to individuals like revolving credits and lines of credits (credit cards, overdraft etc.) and personal term loans and leases (car loans, student loans etc.) are generally considered as retail loans. The same holds for residential mortgage loans when these are granted to the individual owner-occupier of the property. Small business loans are considered as retail loans when the total (consolidated) exposure is less than $1 million. Larger exposures are treated as firms. Each exposure must belong to a large pool of exposures and must be treated consistently on a pooled basis and not as a firm by the bank’s risk management.

The retail asset class is partitioned into 3 subclasses:

- Qualifying revolving retail exposures (QRRE): It concerns revolving, unsecured and uncommitted exposures that are held by individuals that are permitted to borrow up to a limit set by the bank (max $100,000). Within this limit, customers are allowed to borrow and repay at their discretion. Because this portfolio is assigned a low asset correlation, the low loss volatility has to be justified by past loss experience.

- Residential mortgages: Residential mortgages provide funding for the purchase of residential real estate that is purchased by an individual with the purpose to occupy the property.

- Other retail exposures: This category contains all retail exposures that belong neither to qualifying revolving retail exposures nor to residential mortgages.

Note that purchased receivables are categorized either into retail or firm exposures. Specific rules apply for these assets and are applicable to reduce regulatory burden.

- Equity exposures: An equity exposure is defined based upon the economic substance of the investment instrument, which typically includes direct ownership interests with or without voting power. Equity exposures are irredeemable, the invested funds are returned only in the case of a sale or liquidation. They do not embody an obligation to the issuer and convey a residual claim on the assets or income of the issuer. Also, Tier 1 capital instruments and some specific obligations like perpetual obligations and obligations that can be settled in equity shares, are also considered as equity.

- Securitization exposures: There are many types of securitization exposures like investments in asset-backed securities (ABSs) and collateralized debt obligations (CDOs). Exposures may also result from risk mitigants on these exposures, retention of a subordinated tranche and extension of a liquidity facility or credit enhancement. Securitization exposures are described separately from the 5 asset classes described above.

Risk components and risk weights (IRBA)

The risk components and risk weights are defined for the different asset classes- Corporate, sovereign and bank exposures.

In the foundation approach (IRBAf), the bank’s internal estimates for PD are used together with supervisory settings for LGD, EAD and M. Under the advanced approach (IRBA) the bank’s internal estimates for PD, LGD, EAD and the internal effective maturity M is calculated.

The firm risk weight function comes from maturity adjustment and correlation function. The same risk weight function is applicable for the sovereign and bank asset classes. Note that small and medium-size firms have a beneficial risk weighting due to a lower correlation up to 4%.

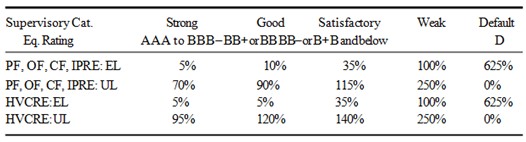

An exception to these rules are the 5 specialized lending subclasses. When the minimum requirements are not met for the estimation of the PD (e.g., because the bank has insufficient data history), the banks can use the supervisory slotting criteria approach that maps the specialized lending assets into 5 supervisory categories ranging from low to high risk. The table below gives an overview of the expected loss (EL) and unexpected loss (UL) risk weights applicable. Higher risk weights are applicable for the high-risk HVCRE segment.

For this asset class, the foundation and advanced IRBA methods are applicable only under strict national regulatory approval, and when a special correlation function is applied in the risk weight function that interpolates between 12% and 30%. National supervisors are allowed to adjust some of the risk weights in the Table within defined ranges.

Table: Supervisory categories, corresponding rating grades, expected loss (EL) and unexpected loss (UL) risk weights for specialized lending exposures with the slotting approach. The expected loss is obtained as 8% of the EL risk weight.