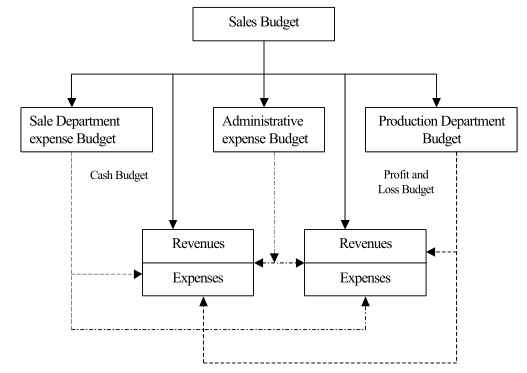

Everything starts with the sales budget, described earlier. From it, data flow in five directions. Figure shows the flow of information from one budget to another. The sales budget provides the basis for the various sales department budgets, such as advertising, selling expenses, and sales office expenses. Sales budget figures also flow directly to the production department. Here the total production budget is established, and from that the various materials and labor budgets are determined. The financial officer also uses anticipated sales figures from the sales budget to prepare the cash and the profit and loss budgets. The cash budget is a tool used to determine how many dollars will flow into and out of the firm each month. This budget is necessary because of the time lag between expenditure and receipt of funds. It is necessary to layout money for materials, labor, advertising, and selling expenses many months prior to selling the merchandise. Then, after sales of the goods, it may he several months before the firm receives cash. The financial officer must ensure that the firm has sufficient cash to enable it to finance the lag between the expenditure and receipt of funds.

The financial officer also uses the anticipated net sales figure as the beginning of the profit and loss budget. The budgets for sales department expenses, production, and general administrative expenses all flow into the profit and loss and cash budgets to determine the expected costs of operation. Thus all budgets are summarized in the profit and loss and cash budgets. Errors in the sales department budgets have a twofold effect on the financial plan. First, the revenues will not be correct. Second, expenses will be out of line because the sales budget determines the production and administrative expenses.