Miller and Modigliani have propounded the MM hypothesis to explain the irrelevance of a firms’ dividend policy. This model, which was based on a few assumptions, sidelined the importance of the dividend policy and its effect thereof on the share price of the firm. According to the model, it is only the firms’ investment policy that will have an impact on the share value of the firm and hence should be given more importance.

Modigliani-Miller derived the following three propositions:

- Total market value of a firm is equal to its expected net operating income dividend by the discount rate appropriate to its risk class decided by the market.

- The expected yield on equity is equal to the risk free rate plus a premium determined as per the following equation: Kc = Ko + (Ko– Kd) B/S

- Average cost of capital is not affected by financial decision.

Critical Assumptions

- It is pertinent to look into the assumptions on which this model is based, before going into the details of the model.

- The essence of a perfect market is that all investors are rational. In perfect market condition there is easy access to information and the flotation and the transaction costs do not exist. The securities are infinitely divisible and hence no single investor is large enough to influence the share value.

- It is assumed that there are no taxes, implying that there are no differential tax rates for the dividend income and the capital gains.

- There is a constant dividend policy of firm, which will not change the risk complexion nor the rate of return even in cases where the investments are funded by the retained earnings.

- It was also assumed that the investors are able to forecast the future earnings, the dividends and the share value of the firm with certainty. This assumption was however, dropped out of the model.

Based on these assumptions and using the process of arbitrage Miller and Modigliani have explained the irrelevance of the dividend policy. The process of arbitrage balances or completely

offsets two transactions, which are entered into simultaneously. Arbitrage can be applied to the investments function of the firm. As mentioned earlier, firms have two options for utilizing its after tax profits (i) to retain the earnings and plough back for investment purposes (ii) distribute the earnings as cash dividends. If the firm selects the second option and declares dividend then it will have to raise capital for financing its investment decisions by selling new shares. Here, the arbitrage process will neutralize the increase in the share value due to the cash dividends by the issue of additional shares. This makes the investor indifferent to the dividend earnings and the capital gains since the share value of the firm depends more on the future earnings of the firm, than on its dividend policy. Thus, if there are two firms having similar risk and return profiles the market value of their shares will be similar in spite of different payout ratios.

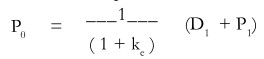

Symbolically the Model is given as

In the first step the market price of the shares is equal to the sum of the present values of the dividend paid and the market price at the end of the period.

Where,

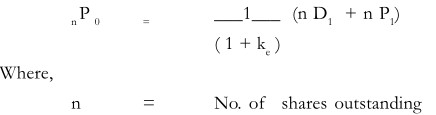

With no external financing the total value of the firm will be as follows:

Now, if the firm finances its investment decisions by rising additional capitals issuing n1 new shares at the end of period ( t = 1), then the capitalized value of the firm will be the sum of the dividends received at the end of the period and the value of the total outstanding shares at the end of the period less the value of the new shares, remains as it is. Thus we have,

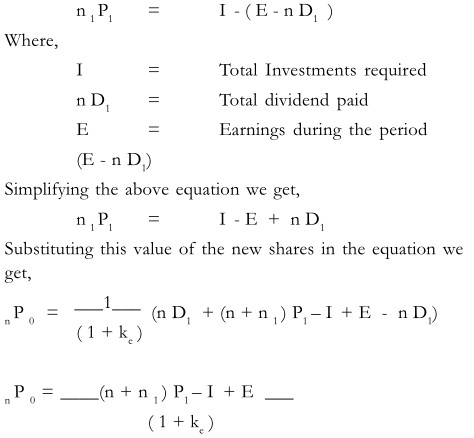

Firms will have to raise additional capital to fund their investment requirements, if its investment requirements are more than its retained earnings, additional equity capital (n 1 P1 ) after utilizing its retained earnings is as follows:

Thus, according to the MM model, the market value of the share is not affected by the dividend policy and this is explicitly shown above.

Critical Analysis of the Assumptions

The MM approach to the irrelevance of dividend has been based on a few assumptions, which need to be evaluated critically especially since a perfect market and absence of flotation costs and transaction costs are situation, which do not happen in reality. Few assumptions have been critically viewed by as under: –

- Tax Effect – This assumption cannot be true, since in the real world the tax rate for the dividend income is higher than the tax rate applicable to the capital gains

- Flotation Costs – The proceeds, which the firm gets from the issue of securities, will be net off the issue expenses. The total issue expenses, which include the underwriting expenses, brokerages, other marketing costs will be around 10 – 15 % of the total issue in India. With the costs of mobilizing capital from the primary market being high, these costs cannot be ignored.

- Transaction Costs – This is an unrealistic assumption, since investors do have to incur certain transaction cost like the brokerage expenses while they dispose off their shares. Thus, if the investors are to equate the capital gains to the dividend income, they should sell off the shares at a higher price. In addition to this, the inconvenience and the uncertainty involved in the share price

- Movements make the investors prefer current income by way of dividends to plough back their profits.

- Market Conditions – Sometimes the market conditions do effect the investment decisions of the firm. For instances, though a firm has profit-able investment opportunities, the bad market condition may not allow it to mobilize the funds. IN such cases, the firms will have to depend on the retained earnings and have a low dividend pay-out ratio. IN still other cases, there may be certain sub-standard investment opportunities in which the firm will invest just because there is an easy access to funds from the market.

- Under Pricing Shares – If the company has to raise funds from the market, it will have to sell the shares to the new shareholders at a price that is less than the prevailing market price. Thus, with the shares being under priced the firm will have to sell more shares to replace the dividend amount.

These criticisms and the preferences for current income, uncertain market conditions presence of transaction and flotation costs, under pricing, etc. highlight the shortcomings of the Miller and Modigliani’s dividend irrelevance policy. Thus, the dividend policy of a company does have an effect on its share value.