The different bases of cost classification are:

- By time (Historical, Pre-determined)

- By nature or elements (Material, Labour and Overhead)

- By degree of traceability to the product (Direct, Indirect)

- Association with the product (Product, Period)

- By Changes in activity or volume (Fixed, Variable, Semi-variable)

- By function (Manufacturing, Administrative, Selling, Research and development, Pre-production)

- Relationship with accounting period (Capital, Revenue)

- Controllability (Controllable, Non-controllable)

- Cost for analytical and decision-making purposes (Opportunity, Sunk, Differential, Joint, Common, Imputed, Out-of-pocket, Marginal, Uniform, Replacement).

- Others (Conversion, Traceable, Normal, Avoidable, Unavoidable, Total)

Classification on the Basis of Time

- Historical Costs: These costs are ascertained after they are incurred. Such costs are available only when the production of a particular thing has already been done. They are objective in nature and can be verified with reference to actual operations.

- Pre-determined Costs: These costs are calculated before they are incurred on the basis of a specification of all factors affecting cost. Such costs may be:

- Estimated costs: Costs are estimated before goods are produced; these are naturally less accurate than standards.

- Standard costs: This is a particular concept and technique. This method involves:

- Setting up predetermined standards for each element of cost and each product;

- Comparison of actual with standard to find variation;

- Pin-pointing the causes of such variances and taking remedial action

Obviously, standard costs, though pre-determined, are arrived with much greater care than estimated costs.

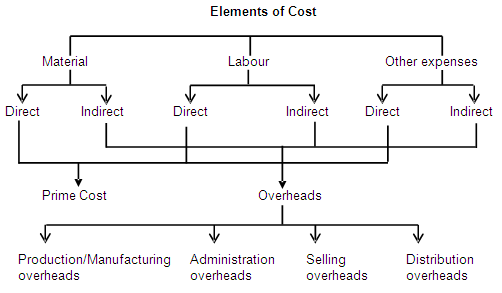

By Nature or Elements

There are three broad elements of costs:

Material: The substance from which the product is made is known as material. It can be direct as well as indirect.

Direct material: It refers to those materials which become a major part of the finished product and can be easily traceable to the units. Direct materials include:

- All materials specifically purchased for a particular job/process.

- All material acquired and latter requisitioned from stores.

- Components purchased or produced.

- Primary packing materials.

- Material passing from one process to another.

Indirect material: All material which is used for purposes ancillary to production and which can be conveniently assigned to specific physical units is termed as indirect materials. Examples, oil, grease, consumable stores, printing and stationary material etc

Labour: Labour cost can be classified into direct labour and indirect labour.

- Direct labour: It is defined as the wages paid to workers who are engaged in the production process whose time can be conveniently and economically traceable to units of products. For example, wages paid to compositors in a printing press, to workers in the foundry in cast iron works etc.

- Indirect labour: Labour employed for the purpose of carrying tasks incidental to goods or services provided, is indirect labour. It cannot be practically traced to specific units of output. Examples, wages of store-keepers, foreman, time-keepers, supervisors, inspectors etc

Expenses: Expenses may be direct or indirect.

- Direct expenses: These expenses are incurred on a specific cost unit and identifiable with the cost unit. Examples are cost of special layout, design or drawings, hiring of a particular tool or equipment for a job; fees paid to consultants in connection with a job etc.

- Indirect expenses: These are expenses which cannot be directly, conveniently and wholly allocated to cost centre or cost units. Examples are rent, rates and taxes, insurance, power, lighting and heating, depreciation etc.

It is to be noted that the term overheads has a wider meaning than the term indirect expenses. Overheads include the cost of indirect material, indirect labour and indirect expenses. Overheads may be classified as (a) production or manufacturing overheads, (b) administration overheads, (c) selling overheads, and (d) distribution overheads.

The various elements of cost can be illustrated by the following chart:

By Degree of Traceability to the Products

Cost can be distinguished as direct and indirect.

- Direct Costs: The direct costs are those which can be easily traceable to a product or costing unit or cost center or some specific activity, e.g. cost of wood for making furniture. It is also called traceable cost.

- Indirect Costs: The indirect costs are difficult to trace to a single product or it is uneconomic to do so. They are common to several products, e.g. salary of a factory manager. It is also called common costs.

Costs may be direct or indirect with respect to a particular division or department. For example, all the costs incurred in the Power House are indirect as far as the main product is concerned but as regards the Power House itself, the fuel cost or supervisory salaries are direct. It is necessary to know the purpose for which cost is being ascertained and whether it is being associated with a product, department or some activity.

Direct cost can be allocated directly to costing unit or cost center. Whereas indirect costs have to be apportioned to different products, if appropriate measurement techniques are not available. These may involve some formula or base which may not be totally correct or exact.

Association with the Product

Cost can be classified as product costs and period costs.

- Product Costs: Product costs are those which are traceable to the product and included in inventory values. In a manufacturing concern it comprises the cost of direct materials, direct labour and manufacturing overheads. Product cost is a full factory cost. Product costs are used for valuing inventories which are shown in the balance sheet as asset till they are sold. The product cost of goods sold is transferred to the cost of goods sold account.

- Period Costs: Period costs are incurred on the basis of time such as rent, salaries, etc.; include many selling and administrative costs essential to keep the business running. Though they are necessary to generate revenue, they are not associated with production; therefore, they cannot be assigned to a product. They are charged to the period in which they are incurred and are treated as expenses.

Selling and administrative costs are treated as period costs for the following reasons:

- Most of these expenses are fixed in nature.

- It is difficult to apportion these costs to products equitably.

- It is difficult to determine the relationship between such cost and the product.

- The benefits accruing from these expenses cannot be easily established.

The net income of a concern is influenced by both product and period costs. Product costs are included in the cost of the product and do not affect income till the product is sold. Period costs are charged to the period in which they are incurred.

By changes in Activity or Volume

Costs can be classified as fixed, variable and semi-variable cost.

- Fixed Costs: The Chartered Institute of Management Accountants, London, defines fixed cost as “the cost which is incurred for a period, and which, within certain output and turnover limits, tends to be unaffected by fluctuations in the levels of activity (output or turnover)”.

These costs are incurred so that physical and human facilities necessary for business operations can be provided. These costs arise due to contractual obligations and management decisions. They arise with the passage of time and not with production and are expressed in terms of time. Examples are rent, property-taxes, insurance, supervisors’ salaries etc.

- Variable Cost: Variable costs are those costs that vary directly and proportionately with the output e.g. direct materials, direct labour. It should be kept in mind that the variable cost per unit is constant but the total cost changes corresponding to the levels of output. It is always expressed in terms of units, not in terms of time.

Management decisions can influence the cost behavior patterns. The concept of variability is relative. If the conditions upon which variability was determined changes, the variability will have to be determined again.

- Semi-fixed (Semi-Variable) costs: Such costs contain fixed and variable elements. Because of the variable element, they fluctuate with volume and because of the fixed element; they do not change in direct proportion to output. Semi-variable costs change in the same direction as that of the output but not in the same proportion. Depreciation is an example; for two shifts working the total depreciation may be only 50% more than that for single shift working. They may change with comparatively small changes in output but not in the same proportion.

Functional Classification of Costs

A company performs a number of functions. Functional costs may be classified as follows:

- Manufacturing/production Costs: It is the cost of operating the manufacturing division of an undertaking. It includes the cost of direct materials, direct labour, direct expenses, packing (primary) cost and all overhead expenses relating to production.

- Administration Costs: They are indirect and cover all expenditure incurred in formulating the policy, directing the organisation and controlling the operation of a concern, which is not related to research, development, production, distribution or selling functions.

- Selling and Distribution Cost: Selling cost is the cost of seeking to create and stimulate demand e.g. advertisements, market research etc. Distribution cost is the expenditure incurred which begins with making the package produced available for dispatch and ends with making the reconditioned packages available for re-use e.g. warehousing, cartage etc. It includes expenditure incurred in transporting articles to central or local storage. Expenditure incurred in moving articles to and from prospective customers as in the case of goods on sale or return basis is also distribution cost.

- Research and Development Costs: They include the cost of discovering new ideas, process, and products by experiment and implementing such results on a commercial basis.

- Pre-production Cost: When a new factory is started or when a new product is introduced, certain expenses are incurred. There are trial runs. Such costs are termed as pre-production costs and treated as deferred revenue expenditure. They are charged to the cost of future production.

Relationship with Accounting Period

Costs can be capital and revenue. Capital expenditure provides benefit to future period and is classified as an asset. On the other hand, revenue expenditure benefits only the current period and is treated as an expense. As and when an asset is written off, capital expenses to that extent becomes cost. Only when capital and revenue is properly differentiated, the income of a particular period can be correctly determined. It is not possible to distinguish between the two under all circumstances.

Controllability

Cost can be Controllable and Non-Controllable.

- Controllable Cost: The Chartered Institute of Management Accountants defines controllable cost as “cost which can be influenced by its budget holder”.

- Non-Controllable Cost: It is the cost which is not subject to control at any level of managerial supervision.

The difference between the terms is very important for the purpose of cost accounting, cost control and responsibility accounting.

A controllable cost can be controlled by a person at a given organizational level. Controllable costs are not totally controllable. Some costs are partly controllable by one person and partly by another e.g., maintenance cost can be controlled by both the production and maintenance manager. The term “controllable costs” is often used to mean variable costs and non-controllable costs as fixed.

Costs for Analytical and Decision Making Process

- Opportunity Costs: Opportunity cost is the cost of selecting one course of action and the losing of other opportunities to carry out that course of action. It is the amount that can be received if the asset is utilized in its next best alternative.

- Sunk Costs: A sunk cost is one that has already been incurred and cannot be avoided by decisions taken in the future. As it refers to past costs, it is called unavoidable cost. The National Association of Accountants (USA) defines a sunk cost as “an expenditure for equipment or productive resources which has no economic relevance to the present decision making process”. This cost is not useful for decision making as all past costs are irrelevant. CIMA defines it as the past cost not taken into account in decision making.

It has also been defined as the difference between the purchase price of an asset and its salvage value.

- Marginal Costs: It is the aggregate of variable costs, i.e., prime cost plus variable overheads. Thus, costs are classified as fixed and variable.