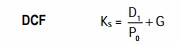

The opportunity cost of the retained earnings (internal equity) is the rate of return on dividends foregone by equity shareholders. The shareholders generally expect dividend and capital gain from their investment. Thus, the shareholders’ required rate of return or the cost of equity is the expected dividend yield and capital gains, Equation (7) can be used to calculate the cost of equity;

Where ke is the cost of equity, DIV expected dividend next year, Po share price today and g expected growth in dividends, The cost of equity is thus equal to the expected dividend yield (DIV / P0) plus capital gain rate as reflected by expected growth in dividends (g). It may be noted that Equation (7) is based on the following assumptions:

- The market price of the ordinary share (Po) is a function of expected dividends.

- The initial dividend DM is positive (DIV,. > 0).

- The dividends grow at a constant rate g, and the growth rate (g) is equal to the return on equity (ROE) times the retention ratio (b) : (that is 9 = ROE x b).

- The dividend payout ratio i.e. (1 – b) is constant.

The cost of retained earnings implies that if the firm would have distributed earnings to shareholders, they could have invested it in the shares of the firm or in the shares of other firms of similar risk at the market price (Po) to earn a rate of return equal to ke Thus, the firm should earn a return on retained funds equal to ke to ensure growth of dividends and share price. If a return less than ke is earned on retained earnings, the market price of the firm’s share will fall. It may be reemphasized that the cost of retained earnings will be equal to the shareholders’ required rate of return. It is the opportunity cost of dividends foregone by shareholders.